Legal Guidebook: How to Invest in Chinese Startups

General step-by-step guide to investment restrictions, deal process, structuring options, and exit considerations for overseas investors in Chinese startups and scale-ups

Huge thanks to Hallam Chow, Runze He, Tim Liu, Yuhang Ma, Fedor Susov, Wei Yuan and other experts for contributing to this article.

Disclaimer:

This article is for general informational purposes as a high-level guidance for foreign investors exploring investments in Chinese startups. None of the information presented in this article constitutes any legal or regulatory advice. Readers should not act or refrain from acting on the basis of any information in this article without first seeking independent professional advice tailored to their specific situation. For clarifications on the exact investment and exit procedures, feel free to contact Haiwen & Partners or any other specialised law firms.

Summary:

Foreigners can invest in Chinese startups that don’t fall into investors’ home country restrictions (export controls), as well as other applicable Chinese laws and regulations, such as the so-called Negative List or National Security Review criteria.

Further stages are similar to such in Western countries: company-level approvals, government reviews for sensitive areas (similar to CFIUS in the US) and closing procedures.

The main difference may be in applicable in capital controls and FX conversions that require additional procedures from the bank.

Chinese startups can be divided in the following groups:

1) the ones with overseas holdcos (e.g. Bytedance) that can be accessed directly at the offshore holdco level;

2) domestic JVs that have both local and foreign shareholders and can accept USD investments (e.g. Unitree) — can also be invested directly – but at the onshore PRC level;

3) domestic RMB-only companies that would not accept foreign investments, but could be accessed indirectly via RMB-denominated intermediary structures (QFLP) established in Mainland China and managed by a local GP.

Offshore holdco is the most straightforward structure for both investment and exit, as the shareholding is built at the offshore level so it doesn’t involve proceeds repatriation from China at the time of the exit. The Chinese regulatory requirements also tend to be lighter. The trade-off, however, is a narrower range of investment targets.

Onshore direct investment provides access to many Chinese deep tech startups, though domestic exits may require additional steps for repatriating proceeds to foreign investors.

Onshore RMB structures (QFLP) offer the broadest coverage of investment targets and are well-suited as a long-term investment solution. While the initial setup requires more effort, the structure can be reused for future investments and provides a more streamlined path for exit repatriation.

“How can we invest in Chinese startups? Is it even legal?”

“How can we exit from our investment in China?”

“When we exit, how do we get our money back?”

These are the questions I often get even from professional investors who are just starting to explore VC investments in China.

Investing in Chinese startups is definitely legal. Moreover, Mainland China was the world’s 2nd largest destination of foreign direct investments (FDI) in 2024 (UNCTAD).

But there are a few aspects that a global investor should consider before investing in a Chinese startup:

industry restrictions,

investment structure,

profit (i.e. exit proceeds) repatriation.

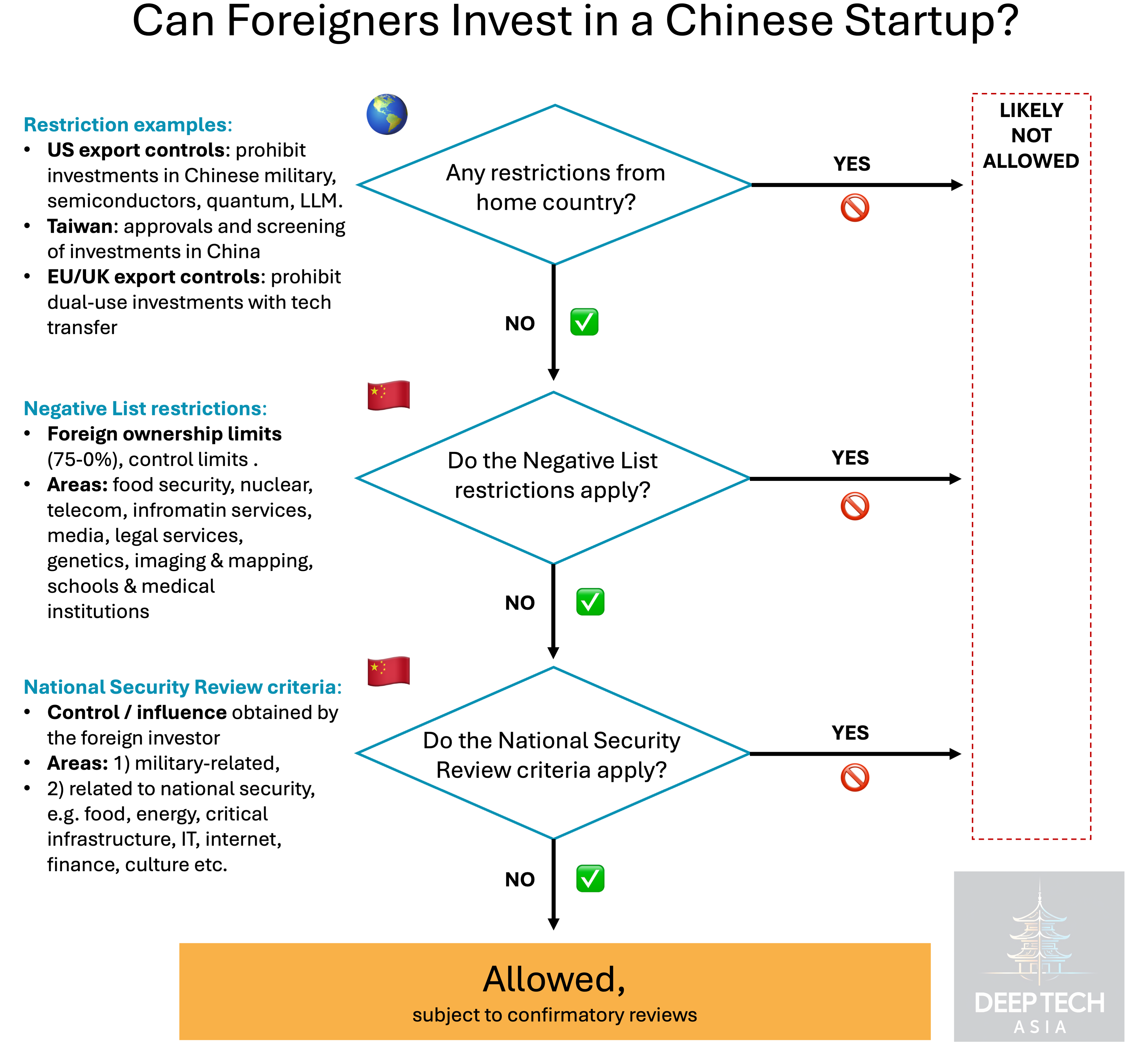

The first thing after identifying your potential investment target in China is to determine whether you as a foreigner are allowed to invest in this startup.

There are three main considerations that may limit your investment:

Restrictions from your home country. These are mainly export control rules. The most strict ones are imposed by the US government which restricts US citizens from investing in Chinese dual use, semiconductor, quantum and LLM companies (Outbound Investment Security Program). Export controls in the EU, UK and other Western countries apply mostly to investments in dual use companies that also includes tech transfer. It usually excludes passive minority investments.

China’s Negative List restrictions. Foreign investors are not allowed to own more than a certain percentage of companies in sensitive areas included in the so called Negative List issued by National Development and Reform Commission of the People’s Republic of China (NDRC) and Ministry of Commerce of the People’s Republic of China (MofCom). Some of the areas include:

ICT: telecom, news, media, publishing — i.e. almost any digital platforms,

Space: aerial mapping and imaging, air transport,

Energy: nuclear power plants construction and operation,

Biotech: human stem cells, genetic diagnosis.

Full list is published here (in English).

3. China’s National Security Review criteria. If a foreign investor wishes to get either direct or indirect control or significant influence (e.g. board seat) over a Chinese company which is military-related or related to critical infrastructure (energy, food, IT, finance etc), you need to apply to NDRC for approval. Exact wording here (in English).

If none of the key restrictions apply, you may kick off the investment process.

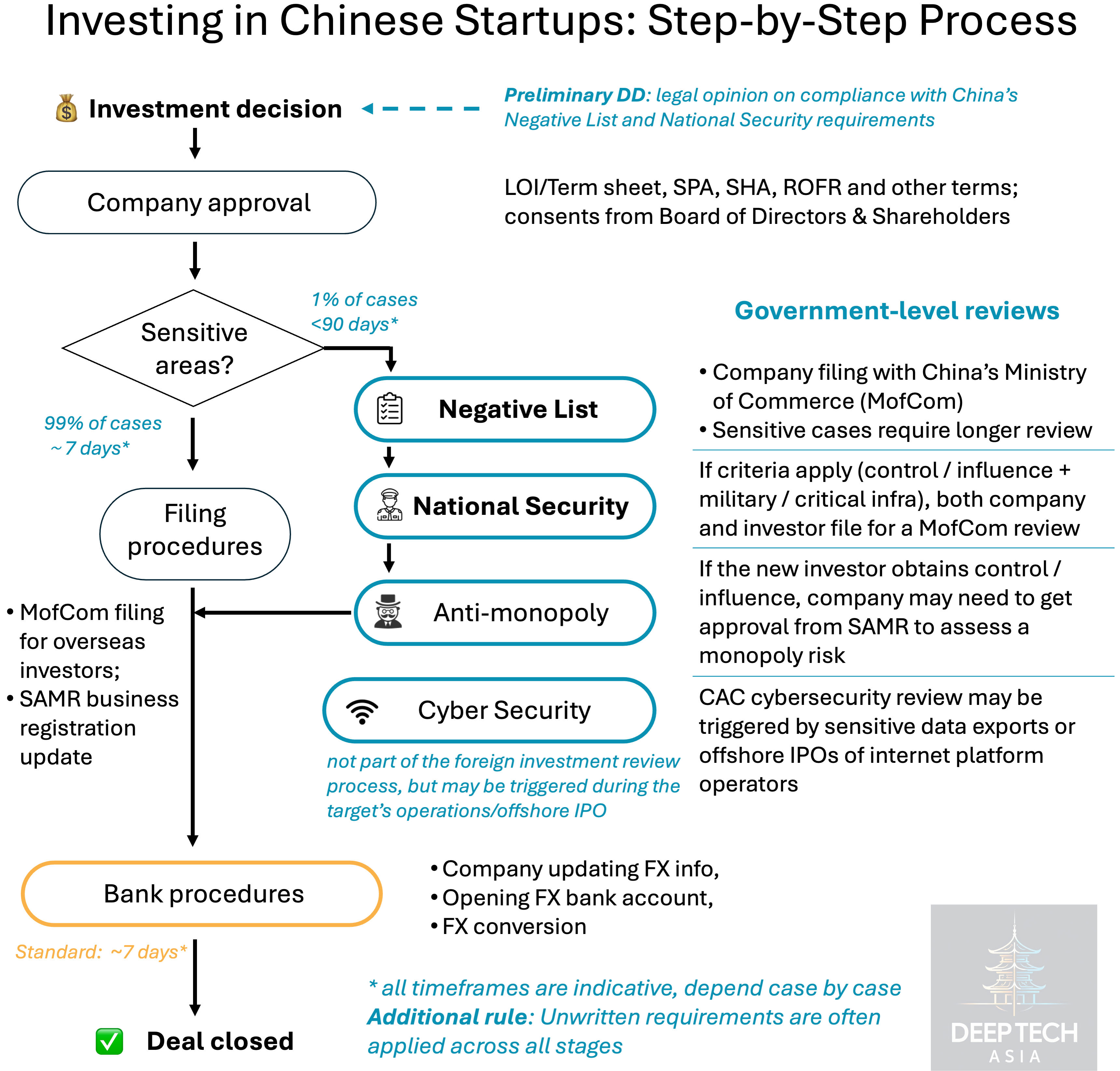

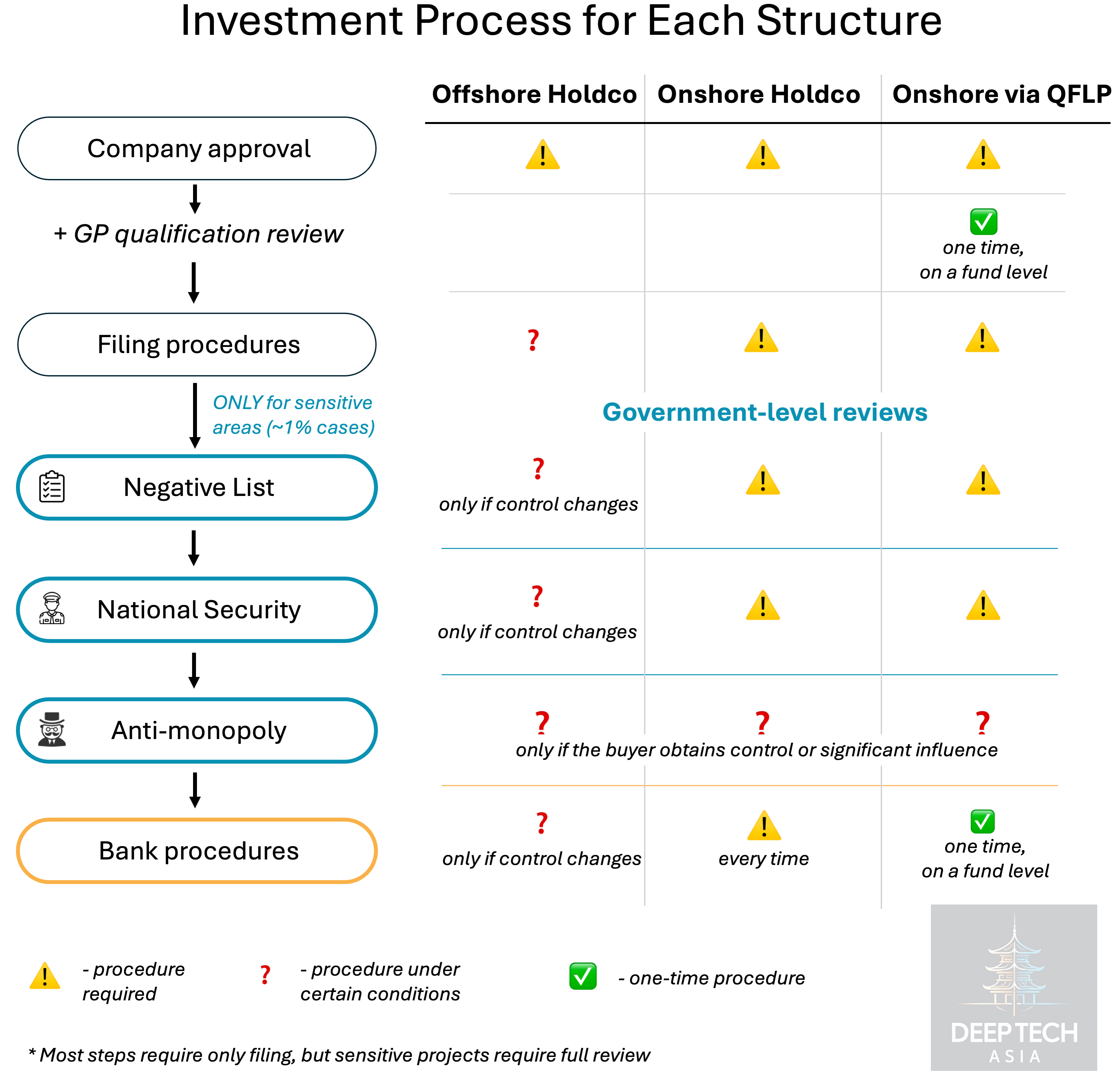

Investment Process

Investment Process

After making an investment decision, there are four main stages of the investment process:

Company-level approvals (LOI/Term Sheet, SPA, SHA etc) + consents from the company’s directors and shareholders.

Filing procedures — most target companies only require a simple procedure of issuing register of shareholders, capital contribution certificates or share certificates and updating MofCom and SAMR registers and corporate information, which usually takes around a week.

China’s Governmental approvals — if the target company falls into the Negative List or in any other sensitive areas, the foreign investor and/or the target needs to obtain approvals from NDRC and/or MofCom (as applicable) and other authorities, such as Cybersecurity Administration of China (CAC) and State Administration for Market Regulation (SAMR).

Bank-level procedures related to China’s capital control rules and foreign currency conversion regulated by the State Administration of Foreign Exchange of the People’s Republic of China (SAFE) should also be considered.

Important to note that unwritten and informal requirements also apply broadly across each stage of the investment process. For example, in some cases you may satisfy all formal requirements, startup founders — especially the most popular ones — may still be reluctant from approving your investment because of various business, regulatory and/or timing considerations.

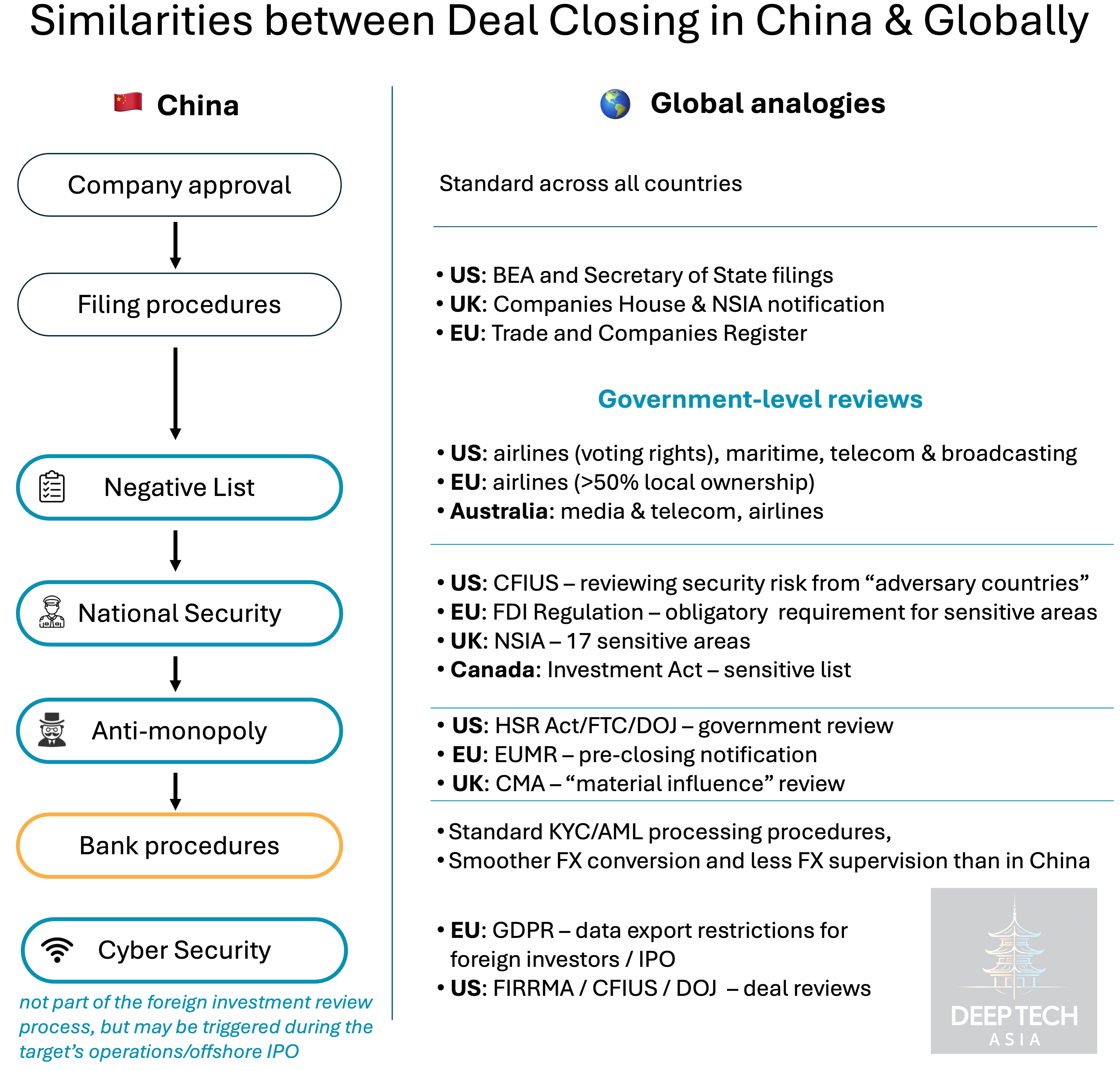

Despite these multiple layers of reviews, investment process in China is not that different from cross-border investments in Western deep tech startups:

Industry-specific restrictions for foreign investors are imposed in most Western countries in areas like airlines, telecom, broadcasting etc.

China’s National Security Review is very similar to the US CFIUS regulation both in terms of the filing procedure and reviewing criteria.

Cybersecurity rules are also similar both in China and US/EU with GDPR and other data export restrictions.

Same goes for anti-monopoly regulation.

Capital controls may be the main difference.

Investment Structures

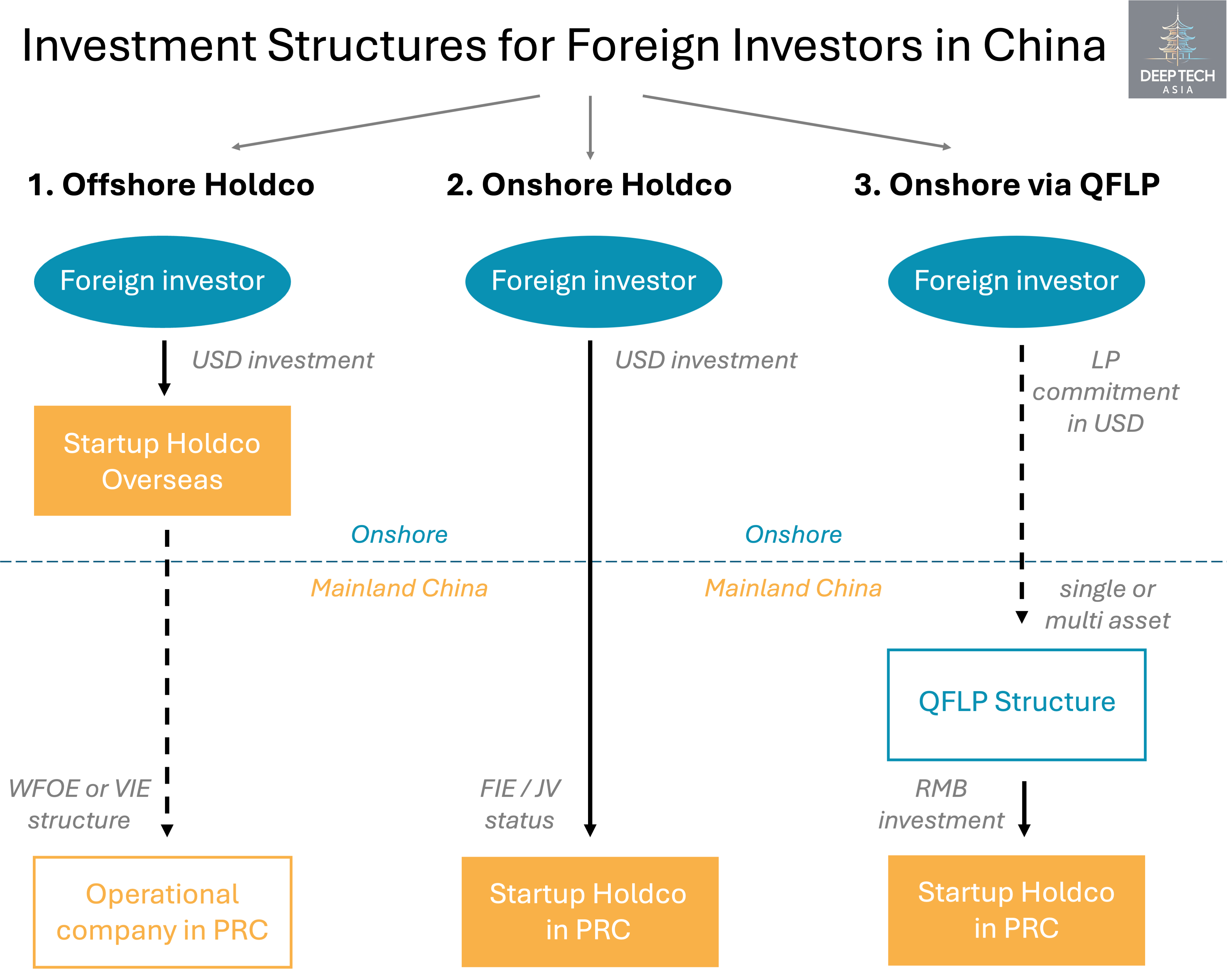

From a corporate structure perspective, Chinese startups can be divided into two groups:

Companies with overseas holdcos (“Red Chips” or “P-Chips”) — “de jure” non-Chinese companies (Cayman, BVI, Hong Kong etc), but with significant operations in Mainland China. These operations are typically linked to the holdco in one of two ways:

WFOE: the foreign holdco directly or indirectly wholly owns the Chinese entity,

VIE: the offshore holdco indirectly holds a WFOE in the PRC and that WFOE obtains contractual control over the VIE company through a series of contractual arrangements. The VIE company itself is typically a purely domestic PRC company held by the founders or other PRC persons, which structure is commonly used in practice in sectors subject to foreign investment restrictions.

Domestic companies incorporated in Mainland China without any overseas holdcos. They are divided into two groups:

Joint Ventures (JVs) — companies with both PRC and foreign investors that are open to receiving foreign investments in USD directly.

RMB-only companies — companies backed exclusively by domestic investors. Although not restricted by the Negative List, they typically avoid foreign capital due to more complex closing procedures and increased regulatory scrutiny. They can accept only RMB investments.

Vast majority of Chinese startups belong to the “RMB-only” category, but most of them — except for the most sensitive ones — can be converted into JVs after admitting a foreign investor. Based on my analysis of cross-border deals, only 11% of investment rounds of Chinese startups in 2025 had at least one foreign investor, which can indirectly indicate an approximate share of JVs among all active startups in China. Only a fraction of all Chinese startups has overseas holdcos, although many of which may be more familiar to foreign investors such as Bytedance, Shein, DJI etc.

Based on each type of startup, various investment structures can be utilised:

If a startup has an overseas holdco, you can invest directly into that holdco entity in USD or other non-RMB currencies and not face any capital control issues at the holdco level.

If it’s a domestic JV company, you have to invest directly into its Mainland Chinese entity which involves the governmental review and capital control procedures. But you would become a direct shareholder of this startup.

If it’s a domestic RMB-only company and it’s not in the Negative List, the only way to invest might be through an onshore RMB structure (fund or single asset vehicle), although it is still subject to approval from the company. To achieve this, most foreign investors use the so-called QFLP structures, although legally you will still be treated as a foreign investor.

VIE structures were widely adopted by Chinese startups — including Alibaba, Tencent, ByteDance, and Shein — during the internet boom of the early 2000s. “Telecom value-added services” and “internet information services” fall under the Negative List as sectors where foreign investment is restricted or prohibited. VIE structures allowed internet startups to bypass those restrictions, raise capital from global investors, and list overseas.

Since 2020, China has introduced new rules that bring VIE structures under greater regulatory oversight. The Foreign Investment Law (2020) and the Trial Measures for the Administration of Overseas Issuance and Listing of Securities by Domestic Enterprises (2023) extended the scope of regulation to include “indirect” foreign investments and introduced obligatory filing of VIE structures with the CSRC (China’s equivalent of the US SEC).

In practice, the Negative List prohibits or restricts foreigners from directly investing in Chinese entities operating in restricted sectors such as certain specified internet services.

Qualified Foreign Limited Partner (QFLP) structure is a regulatory program that lets approved foreign investors commit capital into RMB-denominated PE/VC funds (multi or single asset) established in China. In practice, a foreign LP (or group of foreign LPs) is licensed/qualified under a local QFLP pilot, converts foreign currency into RMB under agreed rules, and then invests through a domestic vehicle managed by a local licensed GP.

After obtaining all licenses and qualifications, the QFLP structure might simplify the investment and repatriation processes for all consequent deals made through the same vehicle, although the first transaction would require even more administrative efforts than a direct investment into an onshore company.

The exact QFLP configurations vary across different city/province-level pilot regimes (e.g., Shanghai, Beijing, Shenzhen, etc.). You can find here a more detailed description of the Shanghai QFLP program.

The investment process is also slightly different for each structure:

Offshore holdco is often the most straightforward structure, as it involves fewer reviews on the China side, unless the investment resulted in the change of the control.

Onshore holdco can involve more PRC regulatory procedures and therefore tends to require the most coordination.

QFLP involves the same level of PRC regulatory procedures as onshore holdcos, but it simplifies the bank procedures for all consequent deals and might potentially provide an access to a larger pool of RMB-only companies.

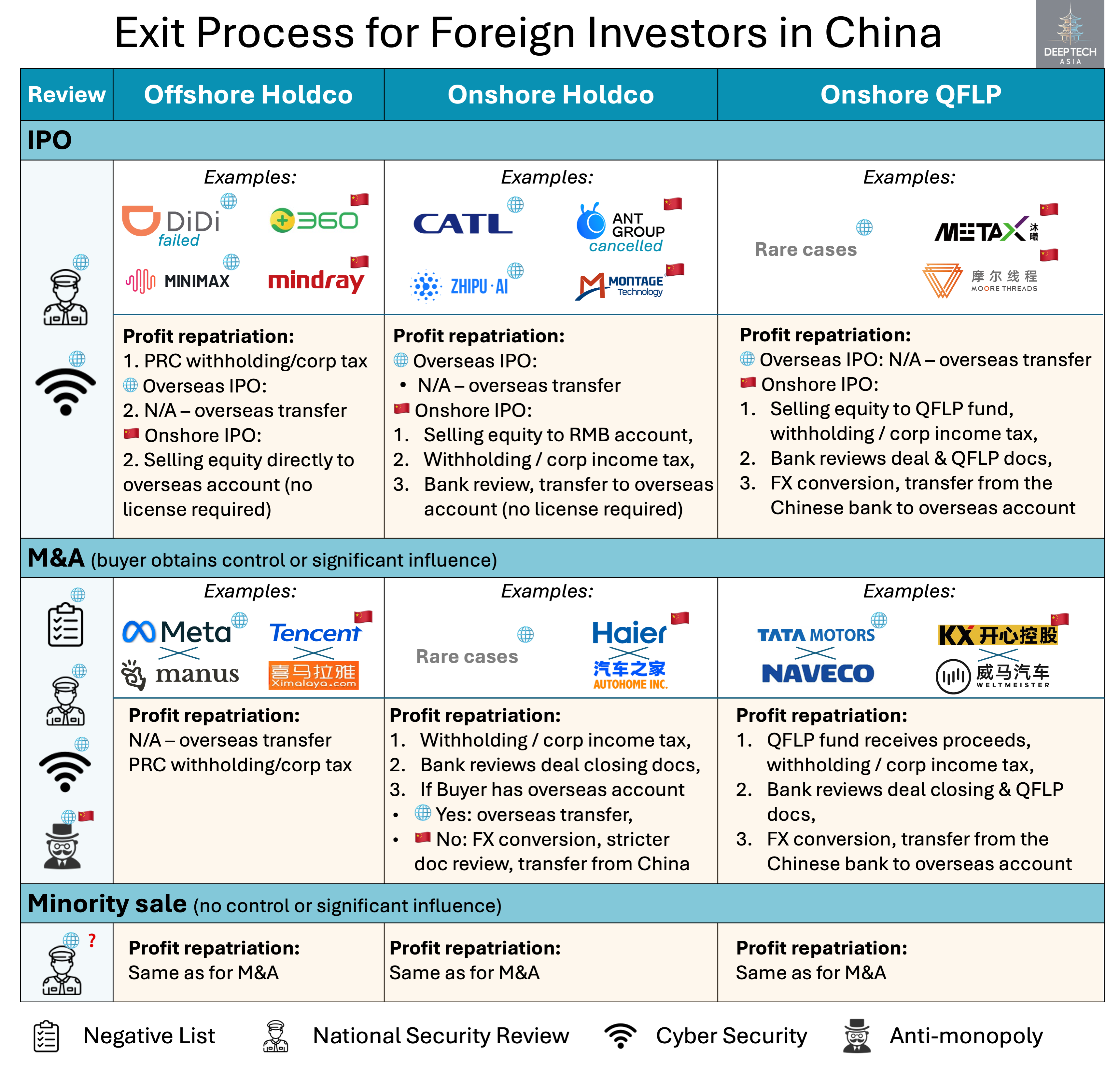

Exit process

Investing in a Chinese startup may not be as hard as exiting from it.

There are three main hurdles for exiting from a Chinese startup, some of which may be by reason of business opportunity and market consideration:

Exit opportunities — IPOs, M&As, secondary private placements.

Government reviews — Negative List, National Security and anti-monopoly regulation.

Capital control rules — profit (i.e. exit proceeds) repatriation.

Below we’ll dive into each of these hurdles.

Exit opportunities

In 2025, China was the second largest VC/PE liquidity market after the US and the trend is positive (more on this in my previous articles here and here).

There are three main exit scenarios from Chinese startups:

IPO is the most common exit path in China which is available for all types of startups: domestic ones (Shanghai, Shenzhen, Beijing) for local companies, offshore ones, like Hong Kong (HKEX) or even US (NASDAQ), for the FIEs and overseas holdcos.

M&A is a less common exit path for Chinese startups. Domestic M&A are more frequent, but usually smaller in sizes. Cross-border tech M&As are rare, so sticking to onshore structures makes it easier to find a potential acquirer.

Minority stake sale in the secondary market, depending on the specific company, industry and/or foreign investor(s) involved, tends to be the easiest exit route for the same company from a commercial perspective, compared with an IPO or M&A, if it does not involve a change of control or influence that could trigger additional scrutiny. That said, each transaction should still be assessed on a case-by-case basis.

Government reviews

These restrictions apply equally to all investment structures: onshore companies and offshore companies with a significant presence in China.

However, they vary across different exit strategies.

Cross-border M&As are the most complex, as they may involve all kinds of security-related governmental reviews depending on both the nature of the acquisition target and the acquirer itself.

An example of this issue may be the Meta acquiring Manus case:

Although Manus is a Singapore-based company, most of its operations have been originated from Mainland China.

In early 2025, the US VC firm Benchmark led the company’s Series B, which hasn’t triggered any significant scrutiny from China, because Benchmark only acquired less than 15% of Manus.

However, when Meta acquires Manus, the change of control prompted scrutiny of export control and/or National Security and Cybersecurity reviews.

IPOs are generally more complex than M&As due to standard disclosure procedures. The most pressing issue with overseas IPOs is usually related to sensitive data export, especially for large consumer platforms, e.g. Didi. Meanwhile, China’s leading LLM player Minimax with ~60 million users in China successfully went public on HKEX in 2025.

A minority stake sale in the secondary market, depending on the specific company, industry and/or foreign investor(s) involved, tends to be generally the easiest exit route for the same company, compared with an IPO or M&A, if it does not involve a change of control or influence that could trigger additional scrutiny. That said, each transaction should still be assessed on a case-by-case basis.

Generally, any cross-border and overseas exits tend to trigger much heavier government scrutiny than domestic exits.

Capital controls & taxation

Capital controls are much easier for cross-border and overseas exits than for pure domestic cases. But different investment structures involve various level of repatriation complexity.

Offshore holdco is the easiest exit structure from the perspective of repatriating the exit proceeds, because your shares are held in an offshore jurisdiction usually with no capital control rules.

If the company is acquired, the acquirer usually can transfer your money directly from a dedicated overseas bank account.

If the startup goes public outside of Mainland China, you can sell your shares on the global public markets after the lock-up period.

The only complication may arise when the global entity goes public in Mainland China, which is rare. In this case, after the expiration of the lock-up period you can sell your public equities as a pre-IPO investor on the onshore stock exchange without any additional license (e.g. QFII) if the transaction is only for the exit purpose. After that the proceeds first go to your dedicated RMB account. Then after settling the withholding on the corporate income tax (10% for non-residents) and undergoing a bank review, the exit proceeds can be transferred to your overseas account.

Worth noting that under China’s tax regulation, exiting from overseas companies may be considered as an overseas indirect transfer if the company’s actual business originates mostly from China. Under Bulletin 7 and relevant rules, such an indirect transfer of PRC assets by a non-PRC tax resident may be re-characterized as a direct transfer of PRC taxable assets if the transaction lacks reasonable commercial purposes. In this case, PRC-sourced gains from the transfer may be subject to enterprise income tax, and tax filing and withholding obligations may be triggered — effectively making the deal taxable in the same way as exiting from a domestic Chinese company.

Domestic holdcos (both direct and via QFLP) require more administrative steps for repatriation, as investors need to complete bank documentation reviews for each transaction before transferring the exit proceeds out of China — a process that, while standard, can add time and complexity compared to offshore structures.

If your shares are acquired by a foreign buyer with an overseas bank account, it is theoretically possible to request the buyer to transfer the exit proceeds directly to your overseas bank account to avoid repatriation issues. However, this may still require paying the withholding on the corporate income tax which must be settled onshore in RMB.

In case of IPO, same as for overseas holdocs, if the company is going public overseas, you can sell your shares after the lock-up period and transfer money directly to your account.

If the company goes public in Mainland China or if it’s acquired by a local buyer, you need to file repatriation of your proceeds with the Chinese bank. For this, the bank will review transaction documents, including source of income, tax settlement confirmation, your foreign company information etc. This process is also common for any exit from investment in Western countries, with the exception that no tax clearance confirmation is required.

Onshore QFLP structures involve more upfront steps than investing directly into a Chinese holdco, as both the foreign investors (LPs) and the local GP need to meet additional qualification requirements. However, once the QFLP is established, it may simplifies the repatriation process of exit proceeds for all consequent deals made through the same licensed vehicle.

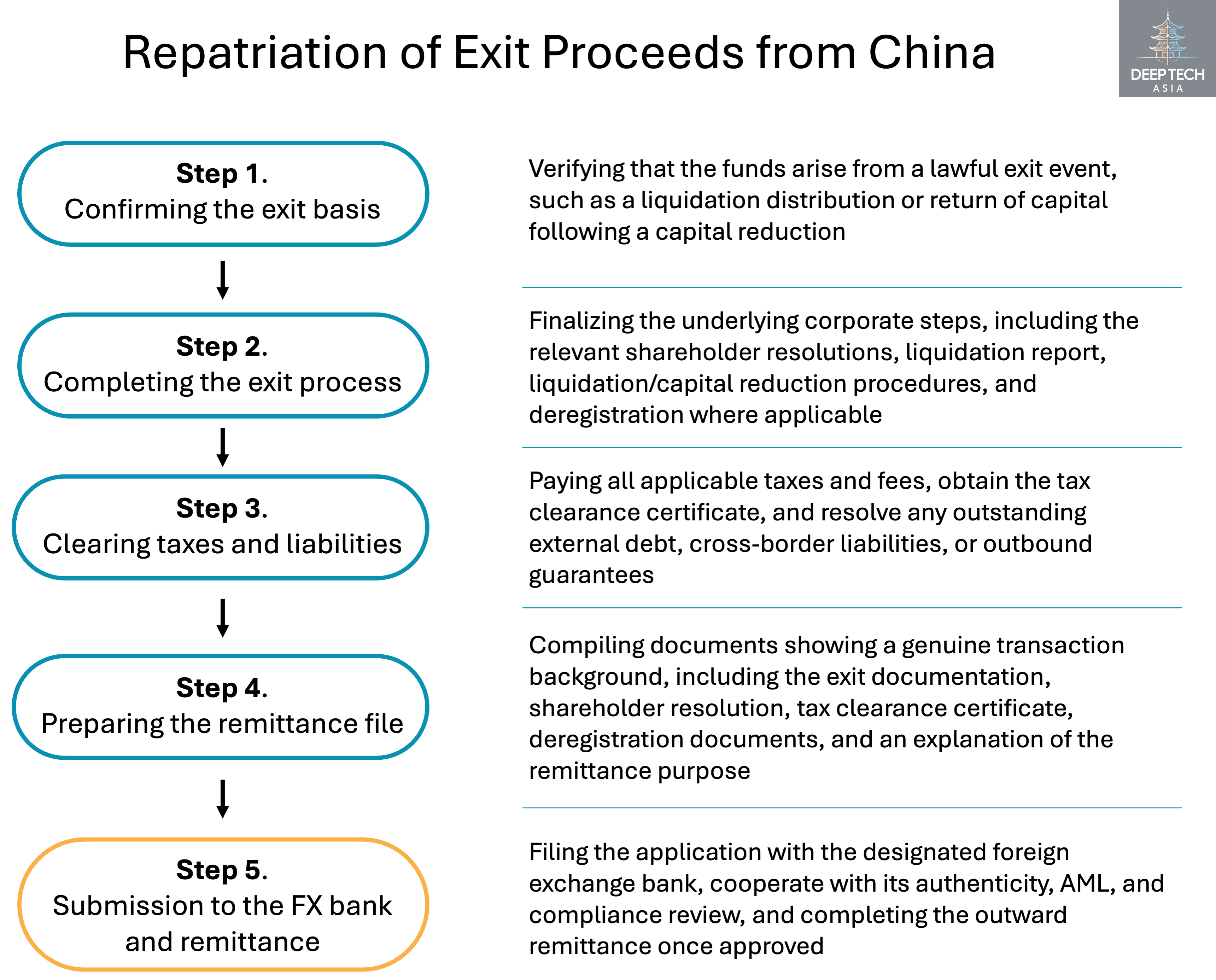

Below is the summary of the step-by-step process of repatriating exit proceeds for foreign investors from selling shares in Chinese onshore entities, based on the guide of K-Bright Law Firm (in Chinese).

Under Article 22 of the Implementing Regulations to the Foreign Investment Law (外商投资法实施条例):

“A foreign investor’s capital contributions made within China, profits, capital gains, proceeds from asset disposals, royalties from licensed intellectual property, compensation or damages lawfully obtained, liquidation proceeds, and the like may be freely remitted into or out of China in RMB or foreign currency in accordance with the law. No entity or individual may illegally restrict the currency, amount, or frequency of such inward or outward remittances.”

In principle, there is no legal barrier preventing a foreign investor from exiting through an equity transfer and remitting its investment returns offshore. In practice, however, the operational requirements of different regulators, complex documentation and various bank review standards require detailed arrangements to reduce potential risks.

This is why engaging a specialised legal advisor during the repatriation of exit proceeds is crucial.

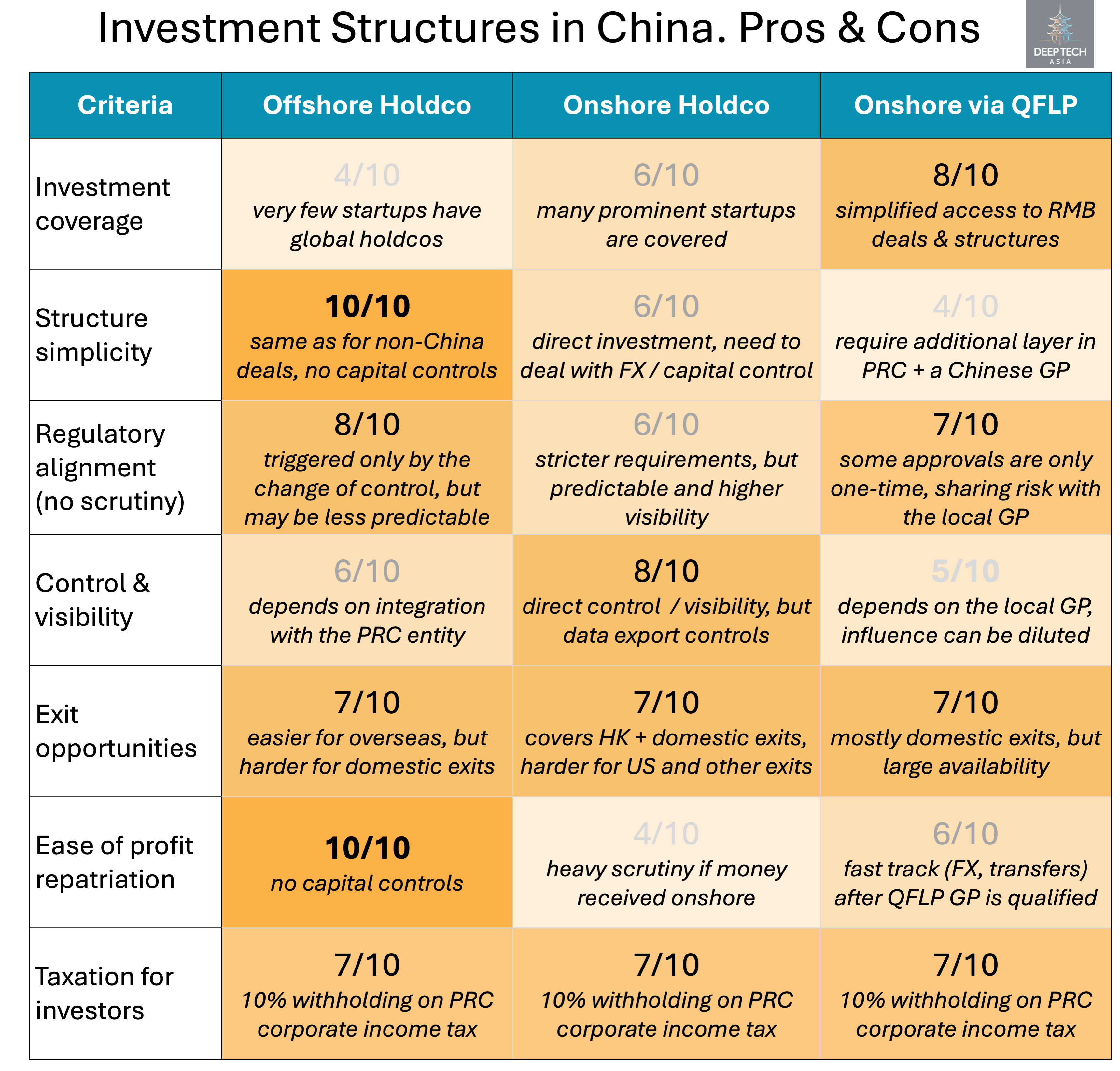

Final remarks: which structure is better?

Everything depends on the goals of the investors:

If you want to make investments in China, offshore holdcos might be the best choice, because they are the easiest to start with, no capital control issues, most target companies are global in nature and well-knows outside of China. They also may be more open to foreign investors. However, the choice of available opportunities is quite limited.

If you are interested in a specific startup that doesn’t have an overseas holdco, investing directly into an onshore holdco can be an option, but may be subject to longer repatriation process with stricter requirements from the banks. In this case, securing a good Chinese tax or legal advisor is always a good idea.

If you are thinking about a broader long-term strategy of investing in Chinese startups, creating your own QFLP structure may be a preferred option, as it might give you higher coverage of investments with potentially more simplified investment and exit procedures for all consequent deals made through the same vehicle.

If you have any proposals, ideas, or feedback, we’d love to hear from you! Feel free to reach out at denis@deeptech.asia or on LinkedIn. Let’s connect and explore how to improve together.