Are Manus-like Companies Still Investable?

The Meta–Manus deal was supposed to validate the “China-origin, global-first” AI playbook. Beijing blocked the deal — but the playbook is not dead, just more nuanced

Summary:

Manus is the perfect case study of the China-linked global AI playbook: Chinese roots, Singapore HQ, global investors, and a US strategic exit.

Beijing blocked the Meta deal, but the playbook is not dead — it just became more nuanced.

The situation is changing fast, but the overall trend is that there are two categories: China+ companies and fully global companies with Chinese roots.

China+ companies remain very much investable: stay Chinese, leverage China’s ecosystem, sell globally, and underwrite China-aligned exits.

Global companies with Chinese roots are also investable, but the bar is higher. Such companies need a clean cut: IP outside China, no critical mainland R&D dependency, clear ownership, and no regulatory leverage for Beijing.

Manus — the perfect case study

Before the Meta deal collapsed, Manus looked like the ideal example of a new generation of China-linked global AI companies targeting global markets:

Chinese founders, global users,

Singapore headquarters,

top-tier international investors,

potential exit to one of the most important US technology companies.

All within less than two years.

In theory, this was the dream version of the playbook: build with Chinese AI talent, move the headquarters offshore, target global users, raise from global investors, and exit to a US strategic.

Manus seemed to prove that this model could work even in one of the most geopolitically sensitive categories: agentic AI.

Then Beijing blocked the deal.

Is the playbook broken?

According to Bloomberg, the company is exploring a new financing round of around $1 billion to unwind its acquisition by Meta. The same startup that was supposed to become one of the most successful global exits for a China-origin AI company may now need new investors to reverse the transaction.

That makes Manus one of the strangest fundraising cases in recent AI history. A company reportedly acquired by Meta for more than $2 billion is now trying to restructure itself because Beijing decided that the deal should not have happened.

So the question for new investors is no longer simply whether Manus is a good AI company.

The question is:

What exactly are investors underwriting if the most obvious exit path has just been blocked?

And the broader question:

Are global AI companies with Chinese roots still investable?

My answer is yes.

But only if investors understand that the playbook has changed.

The problem is not that a company has Chinese roots. The problem starts when a company wants to be treated as non-Chinese, while its core technology, IP, R&D or regulatory exposure still remains connected to China.

That is the real lesson of Manus.

Lesson for founders

The situation around Manus is still very dynamic, but the overall trend is that there are two kinds of global "China-linked" companies:

1. China+ companies (e.g. DJI, Unitree Robotics, CATL) — company is Chinese, supply chain is Chinese, but the market is global.

2. Global companies with Chinese roots — company leverages Chinese tech and talent, but position themselves as "non-Chinese".

The founders of China-linked companies should honestly answer the question:

Are you a China+ company or a global (non-Chinese!) company with Chinese roots?

China+ companies

These are companies that remain clearly Chinese, but sell globally. There are plenty examples both in hardware (DJI, CATL, Unitree and software (Tencent, Alibaba, Bytedance, Deepseek). The company is Chinese, the supply chain is Chinese, the R&D base is often Chinese, but the market is global.

This model is clear. The company does not pretend to be non-Chinese. It directly leverages China’s strengths: engineering speed, manufacturing scale, supply-chain density, hardware iteration, cost efficiency and increasingly liquid local capital markets.

For China+ companies, the playbook is straightforward: stay Chinese, use the domestic ecosystem, raise from Chinese or China-friendly global investors, expand globally where possible, and underwrite China-aligned liquidity as the base case.

The exit does not need to be a US strategic acquisition. It can be a Hong Kong IPO, a mainland IPO, a domestic M&A transaction, or another exit route aligned with China’s strategic interests.

This model is still very investable. In fact, it may be becoming more investable.

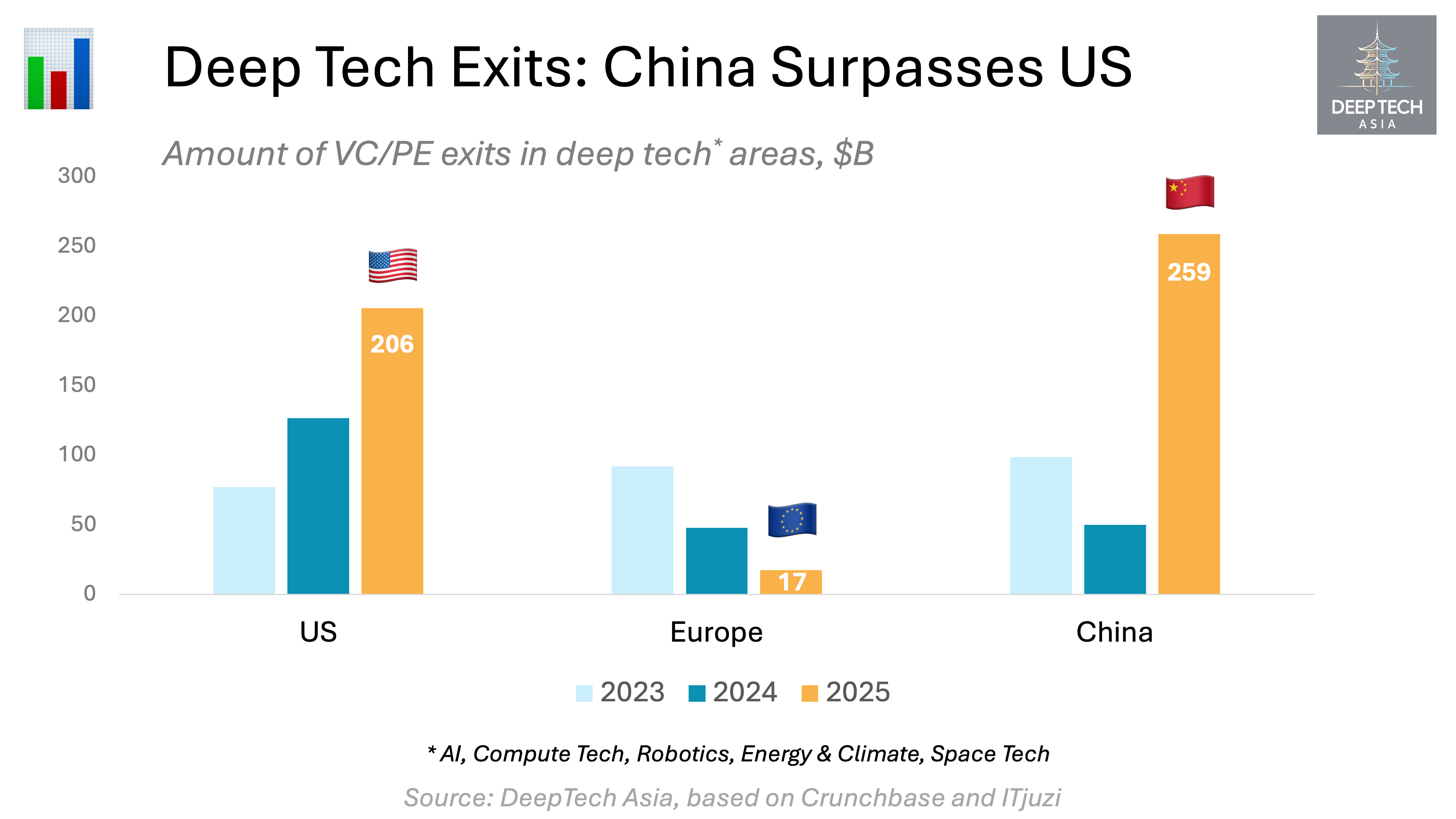

China’s deep tech exit market has improved significantly. In 2025, VC/PE exits in China tripled year-on-year. Total VC/PE exit value reached around $446 billion, roughly half the US level of $894 billion, and far ahead of Europe’s $114 billion. Deep tech exits across AI, compute, robotics, energy and space reached around $259 billion in China, surpassing the US at around $206 billion.

Fully global companies

These are companies like Manus:

leveraging Chinese founder talent, Chinese engineering culture,

positioning themselves as genuinely global and non-Chinese,

HQ is in Singapore, US, Europe, Australia — but not in China,

targeting global customers from day one,

raising from global (mostly US) investors,

exiting globally (mostly in the US).

Chinese founders can absolutely build global AI companies. Chinese engineers can absolutely create world-class products outside China. A company should not be penalized simply because the founder is Chinese or because the team has Chinese background.

But if a company wants to be treated as fully global, it needs to make a clean cut early.

The IP should be created outside China. The core R&D team should be outside China. The company should not depend on mainland operations for critical technology development. The ownership structure should be clear, the cap table should be aligned with the intended exit path, and any historical China connection should be documented rather than hidden.

The point is not that founders need to erase their background. The point is that the company’s technology, control and regulatory perimeter need to match the exit story.

If the desired exit is a US strategic acquisition, investors need to ask from day one: would this company pass a geopolitical diligence process? Would Chinese regulators have any basis to intervene? Could the IP transfer history be challenged? Would a change of control trigger national security concerns?

Manus was caught between the two models

In terms of positioning, Manus looked like a fully global company. It moved its headquarters from Beijing to Singapore, targeted global users, raised from international investors, and pursued an exit to Meta.

But in terms of substance, Manus still had China-linked attributes. Its IP and technology were reportedly originally created in China. Its founder and early operating history were connected to China.

This combination may have been acceptable in the mobile internet era. It is much harder in the AI era.

Now geopolitical tensions and technological rivalry between the US and China are more fierce than ten years ago. And AI is now considered strategic infrastructure. It touches productivity, national security, military applications, data, talent, compute and software sovereignty.

Both countries are moving in the same direction: less tolerance for ambiguity in strategic technology ownership.

Washington is restricting capital, chips, talent flows and sensitive technology transfer to China. Beijing is now showing that it can also restrict the outward transfer of Chinese-origin AI assets.

Global investors are caught in the middle.

Lesson for investors

After Manus, investors in global China-linked companies need to underwrite two things more explicitly:

Exit route. Is the likely exit a US strategic, a Hong Kong IPO, a domestic China listing, an Asian strategic, a European buyer, or a long-term standalone company?

US is still the largest VC exit market, but it’s driven by strategic M&As, which is double sensitive for any China-linked companies.

Regulatory perimeter. Was IP created in China? Could Chinese regulators claim jurisdiction over the technology, founders, IP, data, or historical operations?Investors need clean records showing where the IP was developed, how it was transferred, who contributed to it, what approvals were obtained, and whether any China-origin technology remains inside the company.

If US is the preferred exit path, investors need to make sure that none of the company’s IP or other essential elements were created in China.

Otherwise, it may be fine for raising from US minority investors, but definitely not for strategic M&A exits in the US.

What remains investable

The Manus case does not make China-linked global AI companies uninvestable. It only makes the required playbook much clearer.

China+ companies remain very much investable. These companies stay clearly Chinese, leverage China’s supply chain, R&D base and engineering ecosystem, but sell globally. For them, the right strategy is to raise from Chinese or China-friendly investors, expand internationally where possible, and underwrite China-aligned exits — Hong Kong IPOs, mainland listings, domestic M&A or strategically compatible buyers.

Fully global China-linked companies are also investable, but the bar is much higher. If they want to be treated as non-Chinese, they need to be global in substance: IP developed outside China, no critical mainland R&D dependency, clear ownership and control, and no regulatory leverage for China to intervene at financing, acquisition or IPO.

The problem is not China linkage itself.

The problem is ambiguity.

Both categories remain investable — but only when they are distinct.

If you have any proposals, ideas, or feedback, we’d love to hear from you! Feel free to reach out at denis@deeptech.asia or on LinkedIn. Let’s connect and explore how to improve together.